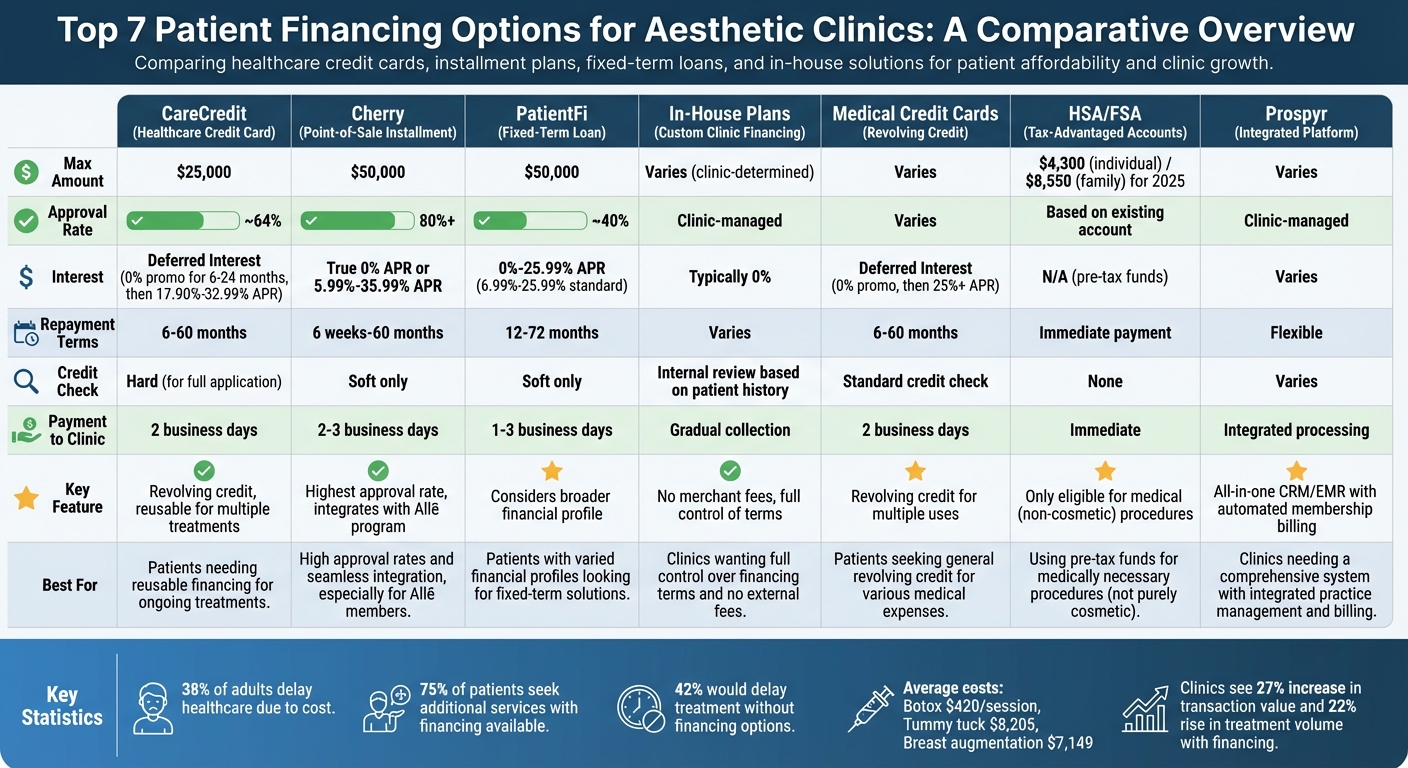

Patient financing makes aesthetic treatments more affordable by breaking costs into manageable payments. With procedures like Botox ($420/session) and tummy tucks ($8,205) often paid out-of-pocket, offering financing options helps clinics attract more patients, reduce cost barriers, and improve cash flow. Common solutions include third-party providers like CareCredit, Cherry, and PatientFi, in-house payment plans, and medical credit cards. Each option varies in terms of approval rates, interest terms, and repayment flexibility, allowing clinics to cater to different patient needs.

Here’s a quick comparison of the top options:

| Provider | Type | Max Amount | Approval Rate | Interest | Repayment Terms |

|---|---|---|---|---|---|

| CareCredit | Healthcare Credit Card | $25,000 | ~64% | Deferred Interest | 6–60 months |

| Cherry | Point-of-Sale Installment | $50,000 | 80%+ | True 0% or 5.99–35.99% APR | 6 weeks–60 months |

| PatientFi | Fixed-Term Loan | $50,000 | ~40% | 0%–25.99% APR | 12–72 months |

| In-House Plans | Custom Clinic Financing | Varies | Clinic-Managed | Typically 0% | Varies |

| Medical Credit Cards | Revolving Credit | Varies | Varies | Deferred Interest | 6–60 months |

Third-party financing like CareCredit and Cherry ensures clinics get paid upfront, while in-house plans require clinics to manage collections. Options like PatientFi and Cherry use soft credit checks, making them patient-friendly. Clinics should choose based on their resources, patient demographics, and treatment types.

Comparison of Top 7 Patient Financing Options for Aesthetic Clinics

How Patient Financing Works in Aesthetic Clinics

Patient financing typically begins with a digital application process, which can be accessed via mobile devices, QR codes, or online links. Providers like Cherry, PatientFi, and CareCredit make it easy for patients to prequalify using a soft credit check - this doesn’t impact their credit score. However, applying for a traditional credit card, such as CareCredit, might involve a hard credit inquiry. Once the application is submitted, approvals are often instant, allowing patients to move forward with treatments on the same day. This quick process not only simplifies access to care but also sets the stage for the financing terms offered by different providers.

After approval, the financing company pays the clinic - usually within two business days - while taking on the responsibility of collecting payments from the patient over time. Clinics benefit from this setup as it supports their cash flow, though they do pay a merchant fee for each transaction.

"When your patient or client pays with CareCredit, you get paid directly with no risk or recourse if they delay or default." - CareCredit

Providers like Cherry and PatientFi offer loans of up to $50,000, whereas CareCredit caps its maximum amount at $25,000. Interest rates vary widely, ranging from promotional 0% APR for six to 24 months to rates between 17.90% and 35.99% after the promo period ends. Some lenders, such as Cherry, offer true 0% APR with no retroactive charges, while others may include deferred interest if the balance isn’t paid off within the promotional window.

Approval rates also differ across providers. Cherry boasts an approval rate above 80%, CareCredit approves about 64% of applicants, and PatientFi has a more selective approval rate of around 40%. PatientFi, however, considers a broader financial profile beyond just credit scores, which could allow more patients to qualify under certain circumstances.

| Feature | CareCredit | Cherry | PatientFi |

|---|---|---|---|

| Type | Healthcare Credit Card | Point-of-Sale Installment Plan | Fixed-Term Loan |

| Max Amount | $25,000 | $50,000 | $50,000 |

| Credit Check | Hard (for full application) | Soft only | Soft only |

| Approval Rate | ~64% | 80%+ | ~40% |

| Interest Type | Deferred Interest | True 0% APR available | Deferred Interest |

| Term Lengths | 6 to 60 months | 3 to 60 months | Up to 60 months |

These options highlight the variety of financing solutions available to meet the needs of both patients and clinics. Each product is tailored to deliver convenience and flexibility, helping clinics improve accessibility while maintaining financial stability.

1. CareCredit Healthcare Credit Card

CareCredit combines patient convenience with a practical way for clinics to maintain steady cash flow. It's a revolving healthcare credit card accepted at over 285,000 locations across the U.S. Unlike traditional one-time loans, this card offers a reusable credit line, making it particularly useful for clinics that provide recurring treatments like Botox, dermal fillers, or laser procedures. Let’s take a closer look at its APR options and other features.

Typical APR Range

CareCredit offers promotional 0% interest for purchases over $200, with repayment terms ranging from 6 to 24 months - provided the balance is paid in full during the promotional period. For patients looking for longer-term financing, the card also provides fixed payment plans with reduced APRs:

- 17.90% for 24 months

- 18.90% for 36 months

- 19.90% for 48 months

- 20.90% for 60 months (for purchases of $1,000 or more)

The standard APR for new accounts is 32.99% as of May 30, 2024.

Loan/Credit Limits and Terms

Credit limits are determined by the applicant’s creditworthiness, and cardholders can request increases through the mobile app or by phone. The card offers tiered financing options:

- Purchases of $200+ qualify for short-term, no-interest plans.

- Purchases of $1,000+ are eligible for 24–48-month reduced APR plans.

- Purchases of $2,500+ can be financed with a 60-month reduced APR plan.

Patients also have the flexibility to combine CareCredit with other payment methods or use it for multiple procedures simultaneously.

Approval Process and Credit Check Type

The approval process is quick and patient-friendly. Patients can prequalify in real time with a soft credit pull, which doesn’t impact their credit score. Once they formally apply, an instant decision is provided, and approved patients can begin using the card immediately. CareCredit’s accessibility is reflected in its 12 million open cardholder accounts, accommodating a wide range of credit profiles.

Integration and Workflow Compatibility

CareCredit’s seamless integration with many practice management software systems, electronic health records, and customer relationship management platforms simplifies the financing process for clinics. Payments are sent directly to clinics within two business days, while CareCredit handles billing and collections. However, clinics must manually select the promotional financing options they want to offer through the CareCredit Provider Center, as not all terms are automatically included.

2. Cherry Point-of-Sale Installment Plans

Cherry provides an appealing financing option with its "true 0% APR" plans that come with no deferred interest. For those who prefer longer repayment terms, interest-bearing plans are available starting at just 5.99% APR.

Typical APR Range

Cherry's APR options are tailored to a patient's credit profile and chosen repayment term. Eligible patients can take advantage of 0% APR for shorter repayment periods. For those opting for interest-bearing plans, rates range from 5.99% to 35.99%, depending on creditworthiness.

Loan/Credit Limits and Terms

Cherry offers financing up to $50,000, with repayment terms ranging from 6 weeks (via the "Pay-in-4" plan) to as long as 60 months. This allows clinics to provide financing options for everything from small procedures to comprehensive treatment plans. A down payment is required at checkout, which can be made using a credit or debit card.

Approval Process and Credit Check Type

The application process is quick - taking less than 60 seconds - and uses a soft credit check, ensuring no impact on the applicant's credit score. Cherry boasts an impressive approval rate of over 80%, catering to a wide range of credit profiles. Once approved, decisions are instant, and approvals remain valid for 30 days, allowing patients to use their balance for multiple treatments if needed[29,31].

"We closed three deals this weekend! That's an extra $7,500 in revenue that we wouldn't have seen if it wasn't because of y'all." – Orlando SMP, Practice

After approval, Cherry simplifies clinic operations with integrations that make the financing process seamless.

Integration and Workflow Compatibility

Cherry integrates smoothly with the Allē loyalty program (by Allergan Aesthetics), enabling patients to earn points on treatments like BOTOX® and JUVÉDERM® while financing their procedures. It also offers API integrations with existing CRM and POS systems, streamlining the checkout process. Clinics benefit by receiving full payment within 2–3 business days, as Cherry handles billing, autopay, and collections. Many practices have reported a 30% boost in case acceptance rates and a 50% increase in average transaction sizes.

3. PatientFi Cosmetic Procedure Financing

PatientFi offers financing tailored specifically for elective aesthetic procedures, making it a popular choice for aesthetic clinics. With fixed-rate plans and APRs starting as low as 6.99%, it provides flexible payment options. For shorter terms, the platform offers 0% interest for 3- and 6-month full-pay plans, while standard plans extend over 12, 24, or 36 months. Patients opting for treatments like BOTOX® or JUVÉDERM® can stretch repayment terms up to 72 months and benefit from an additional 0.25% APR discount.

Typical APR Range

PatientFi's APRs range between 6.99% and 25.99%. Borrowers appreciate the platform's transparency, as it eliminates hidden fees and avoids daily compounding interest. These features have contributed to high satisfaction ratings among users.

Loan/Credit Limits and Terms

Financing amounts range from $200 to $50,000, with repayment terms spanning 12 to 72 months. This flexibility accommodates both minor treatments and more comprehensive procedures. One practice representative shared their experience:

"PatientFi is easy to use for both the patient and the practice. In just three months, our acceptance rates have increased by 75%."

– Tisha F., Practice Representative

Approval Process and Credit Check Type

The approval process is quick and straightforward. Patients can complete the online application in minutes and receive instant decisions. PatientFi uses a soft credit check, which means the application won't affect the patient’s credit score. Once approved, clinics typically receive the funds within 1 to 3 business days.

Integration and Workflow Compatibility

PatientFi simplifies operations for clinics by providing custom application links and marketing materials to help convert consultations into bookings. It integrates seamlessly with Allergan Aesthetics brands like BOTOX®, JUVÉDERM®, and CoolSculpting®. Additionally, the platform offers practice protection by ensuring no penalties or fees for missed patient payments. Clinics can even request advance funding to match their procedure schedules. These features make PatientFi a practical and efficient financing solution, aligning well with clinic workflows and enhancing the patient experience.

4. In-House Payment Plans and Membership Programs

In-house payment plans give clinics the flexibility to create their own financing terms instead of relying on third-party lenders. This means practices can decide on down payment amounts, set installment schedules, and establish their own approval criteria. These plans often come with 0% interest, making treatments more affordable and reducing the "sticker shock" that can discourage patients from booking services during consultations.

Membership programs work a little differently. They charge patients a flat monthly fee in exchange for a set number of treatments or discounts on services. This subscription-based model not only encourages patient loyalty but also ensures predictable monthly revenue for the clinic. Offering financing options can have a big impact: clinics often see a 27% increase in average transaction value and a 22% rise in treatment volume when cost concerns are addressed. These personalized plans allow clinics to manage approvals internally, often based on the patient’s history with the practice.

Approval Process and Credit Check

Approval for in-house payment plans is usually handled within the clinic. Instead of running formal credit checks, practices review the patient’s payment history and their overall relationship with the clinic. However, if a payment plan extends beyond 90 days, federal Truth in Lending regulations may classify the clinic as a "lender", which comes with additional compliance requirements.

Integration and Workflow Compatibility

Managing in-house financing can be labor-intensive without the right tools. Clinics either need dedicated staff to handle billing manually or specialized software to manage recurring payments and keep records organized. Platforms like Prospyr simplify this process by offering features like automated membership renewals and payment processing for recurring billing. These tools not only make tracking payments easier but also help ensure compliance. While in-house plans avoid merchant fees - a concern for 41% of practices - they require strong cash flow and efficient collection systems to operate smoothly. Automated solutions can be a game-changer for clinics aiming to streamline these processes.

sbb-itb-02f5876

5. Medical Credit Cards and General Consumer Financing

Medical credit cards provide revolving credit specifically for cosmetic procedures that insurance typically doesn’t cover. On the other hand, general consumer financing options - like installment loans and Buy Now, Pay Later (BNPL) plans - allow patients to pay off treatments in fixed installments. A key difference with medical credit cards is their revolving credit feature, meaning patients can reuse the card for future treatments without needing to reapply.

One big advantage for clinics is the quick payment process. Financing companies pay providers in full within two business days, ensuring a reliable cash flow. This eliminates the hassle of chasing payments and helps practices maintain financial stability.

These financing options come with specific terms and application processes worth understanding.

Typical APR Range

Interest rates for medical credit cards and consumer financing options can be high. Many medical credit cards start with promotional 0% APR periods, but if the balance isn’t cleared within the promotional timeframe - usually 6 to 24 months - interest rates can soar past 25%. What’s more, interest is often applied retroactively to the entire original amount if the balance remains unpaid. The Consumer Financial Protection Bureau highlights this risk:

"The interest charge on medical credit cards is often deferred for a period of time... if you make late payments or have an unpaid balance once this promotional period ends, you may end up with significant interest and fees on top of your medical bills."

Loan/Credit Limits and Terms

Medical credit cards generally come with lower credit limits compared to personal loans, but BNPL plans and other consumer financing options can go as high as $50,000. Common promotional terms include 6, 12, 18, or 24 months with no interest if paid in full. For more expensive procedures, extended payment terms - ranging from 24 to 60 months - are available with reduced APRs. Considering that procedures like breast augmentation average $7,149 and tummy tucks cost $8,205, these longer-term plans can make high-cost treatments more manageable for patients.

Approval Process and Credit Check Type

Most medical credit cards require a credit check, but many now offer prequalification tools that use soft credit pulls, which don’t affect a patient’s credit score. Applications can be completed in-office or via mobile devices, and upon approval, patients gain immediate access to their credit line. However, the formal application process typically involves a standard credit check by the issuing bank.

Integration and Workflow Compatibility

Seamless integration with clinic systems is essential to reduce administrative overhead. Modern medical credit card platforms often link directly with practice management systems, electronic health records, and accounting software, streamlining the entire application and payment process. These integrations enable instant credit decisions and allow patients to book procedures on the same day. While third-party financing eliminates the compliance challenges of in-house plans, clinics should ensure their staff explains the difference between "no interest" and "deferred interest" terms clearly to avoid potential misunderstandings with patients.

6. Health Savings Accounts and Flexible Spending Accounts for Eligible Procedures

Beyond traditional loans and credit cards, tax-advantaged accounts like Health Savings Accounts (HSAs) and Flexible Spending Accounts (FSAs) can help cover qualifying treatments. These accounts allow pre-tax contributions, but they come with specific rules: only procedures aimed at treating, diagnosing, or curing a condition qualify. Cosmetic treatments, unfortunately, don’t make the cut.

For aesthetic clinics, eligible treatments typically include acne medications, dermatological care, and acupuncture. For instance, alopecia treatments may qualify if supported by a Letter of Medical Necessity (LMN) from a physician. However, treatments for common male pattern baldness are excluded. Similarly, procedures like tummy tucks (abdominoplasty) are considered cosmetic and are therefore ineligible. This is particularly important given that 55.7% of private-sector workers in the U.S. are enrolled in High Deductible Health Plans (HDHPs), and 38% of adults delay healthcare due to high out-of-pocket costs. Clinics must clearly outline these eligibility rules to avoid confusion.

To help patients navigate these accounts, clinics can provide detailed receipts and, when applicable, an LMN to support reimbursement claims. It’s worth noting that HSAs roll over annually and require enrollment in an HDHP, while FSAs operate on a "use-it-or-lose-it" basis. For 2025, HSA contribution limits are set at $4,300 for individuals and $8,550 for families, with an additional $1,000 catch-up contribution for those aged 55 and older.

Most HSA and FSA plans come with debit cards for easy payment, but patients should still verify eligibility with their benefits administrator. Clinics can also direct patients to resources that list eligible expenses to make the process smoother.

7. Prospyr

Prospyr takes a fresh approach to financing by combining clinical and financial workflows into a single, unified platform. Unlike traditional third-party financing tools, Prospyr integrates payment management directly within its all-in-one practice management system. This means practices can handle payment processing, membership management, and patient communication without juggling multiple vendors.

Seamless Integration and Workflow Management

Prospyr’s integrated CRM/EMR system simplifies operations by allowing staff to manage treatment plans, schedule appointments, and process payments from a single dashboard. It accommodates both in-person and virtual payments, while its digital patient portal enables patients to manage their plans, save payment methods, and view treatment histories - all in one place.

The platform’s mobile checkout feature lets providers handle consultations, process payments, and schedule follow-ups right from a tablet. This not only streamlines day-to-day tasks but also keeps the focus on delivering quality care.

For practices offering membership programs, Prospyr automates renewals and recurring billing, reducing manual work while ensuring consistent revenue. Plus, its HIPAA-compliant system safeguards both payment and patient data, meeting all necessary regulatory standards.

How to Choose the Right Patient Financing Options

Choosing the best financing options for your patients depends on the type of procedures you offer and the financial profiles of your patients. For instance, high-cost surgeries like tummy tucks (average cost: $8,205) or breast augmentations (average cost: $7,149) may align better with long-term installment loans or medical credit cards offering extended repayment terms. On the other hand, recurring treatments such as Botox (around $420 per session) or dermal fillers (ranging from $707 to $843 per syringe) are often better suited for Buy Now, Pay Later programs or revolving credit options. Understanding the costs of various procedures can help you decide whether long-term loans or revolving credit options are a better fit for your clinic.

When evaluating financing options, it’s also essential to consider your clinic’s ability to manage risks. Deciding between in-house financing and third-party financing comes down to your clinic’s risk tolerance and administrative resources. With in-house financing, you control the payment terms and retain any interest earnings, but you’re also responsible for collections, compliance with the Truth in Lending Act, and absorbing potential losses from unpaid debts. Third-party lenders, such as CareCredit or Cherry Point-of-Sale Installment Plans, take on these administrative tasks and typically pay your clinic within 2–3 business days. However, this convenience comes with merchant fees.

Approval rates are another factor to weigh. For example, Cherry boasts an approval rate exceeding 80%, which is 78% higher than the industry average. This can significantly improve case acceptance rates. Additionally, look for financing partners that use soft credit checks, allowing patients to explore their eligibility without affecting their credit scores.

| Feature | In-House Financing | Third-Party Financing |

|---|---|---|

| Risk | Clinic assumes full liability for defaults. | Lender assumes risk; clinic is paid upfront. |

| Cash Flow | Payments are collected gradually over time. | Clinic typically receives payment within 2–3 days. |

| Administration | Requires dedicated billing and collections. | Lender handles applications and collections. |

| Compliance | Clinic must adhere to TILA and state laws. | Lender manages regulatory requirements. |

| Cost Considerations | No merchant fees, but clinic bears bad debt risks. | Merchant fees apply per transaction. |

Before implementing a financing program, assess your patient flow. If you observe incomplete treatments or patients opting out of procedures due to cost, it might be time to partner with a financing provider with high approval rates. Training your staff to confidently discuss payment options in private, comfortable settings can also make a big difference - role-playing scenarios can help them build the necessary skills. If you’re leaning toward an in-house financing plan, consult an attorney to ensure your documents comply with both federal and state lending regulations.

Conclusion

Flexible financing plays a key role in helping clinics grow while ensuring patients can access the care they need. Breaking treatment costs into manageable monthly payments encourages more patients to move forward with procedures they’ve been considering. With 38% of adults delaying healthcare due to cost and half of all patients struggling with out-of-pocket expenses, offering financing options can make a real difference.

Clinics also see financial benefits. Third-party financing providers typically pay practices in full within two business days, helping to maintain steady cash flow. Additionally, 75% of patients are more likely to seek additional services when flexible financing is available, while 42% would delay treatment without it. This approach not only supports clinic operations but also strengthens patient confidence.

Providing financing options fosters stronger, long-term patient relationships. Patients who find their provider easy to work with are nine times more likely to stay loyal to that practice. Dr. Nicholas Jones of Nip & Tuck Plastic Surgery highlights this impact:

"CareCredit gives people a way to move forward with something they may have wanted for a long period of time".

To maximize the benefits, offer a range of financing solutions. These could include short-term interest-free plans for smaller treatments, longer-term fixed-rate options for major procedures, or in-house membership programs for recurring services. Train your staff to discuss these options confidently and introduce them early in consultations. Promote financing options clearly on your website, social media, and in-office materials. When patients know support is available before they even see the price, they’re more likely to commit to care. By integrating financing seamlessly into your practice management, clinics can create a supportive environment where patients feel valued and cared for. Tools like Prospyr can simplify this process, making it easier to improve patient retention and drive clinic success.

FAQs

How do CareCredit, Cherry, and PatientFi differ for financing aesthetic procedures?

CareCredit, Cherry, and PatientFi each provide different ways to help finance aesthetic treatments, but they vary in how they’re structured, their approval processes, and payment options.

CareCredit functions like a reusable healthcare credit card. It allows you to finance procedures with promotional no-interest terms, as long as the balance is paid in full within a set time frame (such as 6, 12, 18, or 24 months). Plus, you can use it again for future treatments, making it a convenient option for ongoing needs.

Cherry offers flexible loan options with a high approval rate - over 80%. It provides plans like Pay-in-4 installments or 0% APR options, making it accessible for many patients. Cherry uses a soft credit check, which won’t impact your credit score, and is known for straightforward pricing and relatively low fees for providers.

PatientFi is geared toward larger loan amounts for specific procedures. It provides structured monthly payment plans and deferred-interest options. However, it has stricter approval criteria, with an approval rate of about 40%, and typically involves higher fees for providers compared to the other two options.

Each option has its strengths: CareCredit is great for repeat use with promotional financing, Cherry stands out for its flexible and accessible payment plans, and PatientFi is best for those seeking higher loan amounts with fixed-term payments.

What’s the difference between in-house payment plans and third-party financing options?

In-house payment plans let clinics take full charge of the financing process. They can set up payment schedules, collect installments, and even keep any interest earned. This approach gives practices complete control over terms and cash flow. However, it also means they’re responsible for managing credit risks, handling collections, and ensuring compliance with lending regulations - especially if the repayment period goes beyond 90 days.

On the other hand, third-party financing shifts the credit risk and regulatory responsibilities to an external provider. These companies often approve a large number of applicants and offer perks like 0% APR promotions, which can help attract more patients. Clinics receive payment upfront, while patients pay over time. The trade-off? Clinics usually pay a merchant fee and have less control over the overall patient experience.

An all-in-one platform like Prospyr can make life easier for clinics by automating in-house payment management or seamlessly integrating third-party financing. This allows clinics to offer flexible payment options while cutting down on administrative work.

What should aesthetic clinics consider when selecting a patient financing option?

When selecting a patient financing solution, aesthetic clinics should prioritize a few important factors to benefit both their practice and their patients. Start with the cost structure - seek options that offer competitive interest rates, low fees, and promotional perks like no-interest periods. These not only make financing more appealing to patients but also help maintain the clinic’s profitability. It’s also crucial to consider regulatory compliance, as in-house payment plans exceeding 90 days may fall under lending laws. This makes third-party financing a safer and more reliable option.

The application and approval process is another key area to evaluate. A quick, easy-to-navigate process - featuring instant pre-qualification and fast approvals - can improve patient satisfaction and reduce barriers to treatment. Offering clear repayment terms, such as fixed monthly payments and straightforward interest rates, helps patients plan their budgets while minimizing the risk of missed payments. Lastly, choose a solution that offers seamless integration with your clinic’s systems, like scheduling, billing, and patient management tools. This can simplify operations and lighten the administrative load. For example, platforms like Prospyr provide integrated financing tools in a HIPAA-compliant environment, making the process smooth for both clinics and patients.